Understand Before you Are obligated to pay try a collection of mortgage guides from the consumer Monetary Cover Agency (CFPB). They shows home loan candidates brand new steps they have to simply take to open up and you can handle a mortgage membership. It gives more information on the interest rates, and you can teaches you how to find comparable selling to your fund, also.

This will make perfect sense. Home hunters should know what they’re signing up for. And who wants gotcha times or sudden clarifications immediately after it feels (or actually is) too-late so you can straight back out?

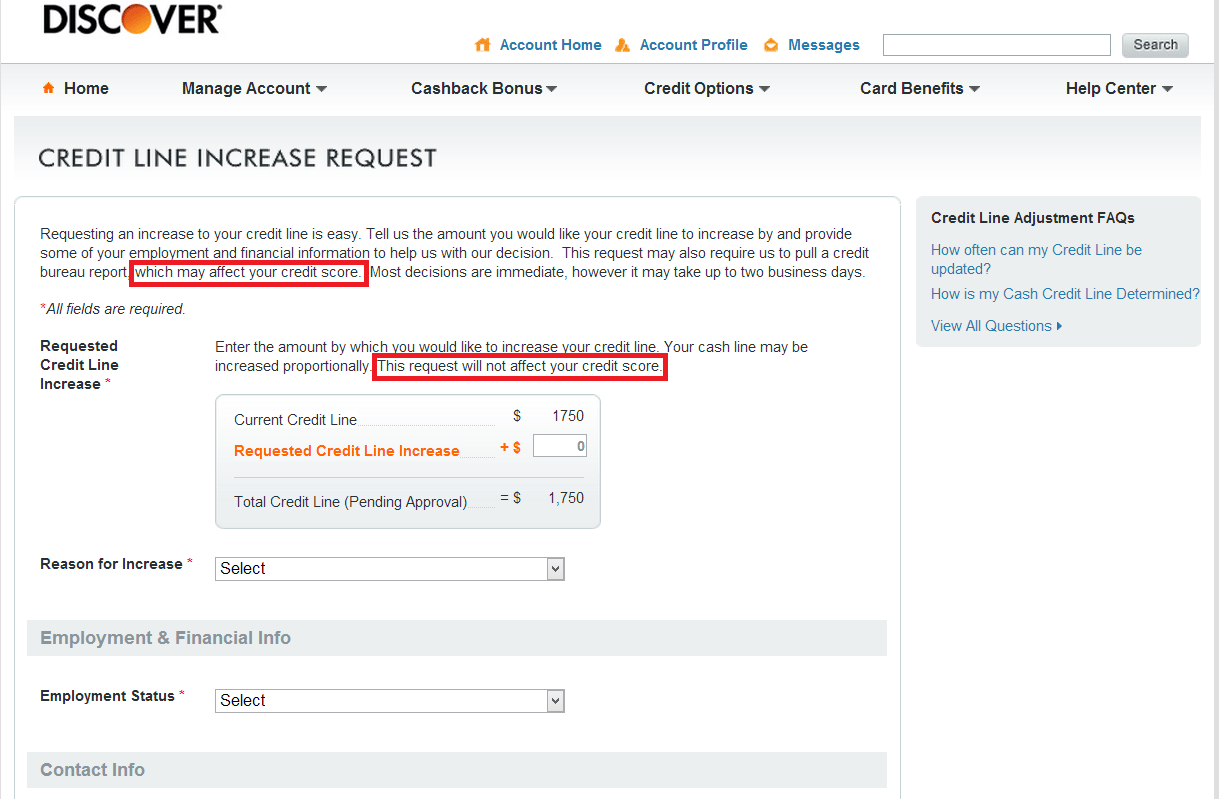

Therefore, the loan lender legitimately have to allow the debtor a proper place away from closure disclosures no less than about three working days in advance of closing day.

Improved Disclosure Product: A reaction to the mortgage Crisis Come out.

Learn Before you could Are obligated to pay assists individuals discover both mortgage process, as well as their choice. The brand new CFPB, a federal institution, actively works to remain lending means reasonable to have regular people. In the agency’s individual terminology: I help to keep banks or any other economic companies consumers depend for each day doing work fairly.

Until the most recent Know Before you could Are obligated to pay package was designed, there have been four disclosure models. These people were not very very easy to comprehend, or even play with.

One to changed following construction drama you to unfolded between 2007 and you will 2010. In reality, new government financial legislation alone altered.

In 2010, the new Dodd-Honest Wall surface Highway Change and you can Individual Cover Work brought loan providers to help you make financing standards more strict, so you’re able to slow down the threats so you can individuals. Because of the 2015, the new CFPB had their very first See Before you Are obligated to pay courses. They simplistic the loan revelation content that the loan providers was required to render their borrowers.

Home loan Disclosures Are simple to Read, Easy to use-And Custom to possess Loan Buyers.

Today, brand new CFPB web site includes their Owning a home part. Which part of the web site guides new hopeful loan borrower as a consequence of the borrowed funds-seeking to excitement. It offers info, guidance, and you can alerts.

- The mortgage Guess. This shows the latest arrangement the buyer try and then make – details of the mortgage and all of the appropriate charges. It states the rate, and you will whether or not that is closed within the. In the event your words punish consumers who pay the month-to-month matter early, which document claims very. The advised, the loan Imagine will help that loan candidate know precisely payday loan Fairfield what is up for grabs, then comparison shop and you can contrast offered mortgages over the past period leading up to closing day! See what that loan Guess works out.

- The fresh new Closing Disclosure. This helps you stop high priced unexpected situations at closure desk. Does the loan Guess satisfy the Closure Disclosure? Brand new toolkit reveals the reader tips compare that it document – their quantity and financing terms – to your same info in which they look towards the Loan Guess. The brand new debtor becomes around three working days examine these models and seek advice before you go done with the newest closure. See what an ending Revelation turns out.

The house Financing Toolkit gives individuals the required context to know this type of disclosures. Plus the mortgage company gets you to definitely for every single borrower. See just what the house Financing Toolkit (PDF) turns out.

Discover The Legal rights, and you may Be aware of the Rules, this new CFPB States

Think about, most of the financial debtor is actually permitted a closing Revelation at the very least around three business days before the deed transfer. This might seem like a pain to have an optimistic client going to the finishing line. But, as you can today pick, you will find a customer-amicable rationale for the around three-time months. It allows buyers to improve their brains regarding the closure in the event the something’s significantly less promised. It includes a flat day whenever a property buyer may get clarifications with the processes and also the terminology, describe questions or confusion, or maybe even request change on the home loan contract.

During the time, the newest agency’s on line book can be extremely of use, even for a skilled client. It offers worksheets, finances forms, plus attempt part-to experience programs the buyer are able to use to prepare the real deal conversations towards mortgage company.

Additionally says to members exactly what financial scam is, and why not to get it done. Claiming well-known? Yes, however people would fudge quantity, therefore perhaps they do need to be told it will most likely not stop better!

Mortgage Companies Must Approve People into the a completely independent Ways. Therefore Must Their Application!

Within the , the CFPB granted suggestions to help you lenders towards the using formulas, along with artificial cleverness (AI). Cutting-edge technical tends to make a myriad of consumer studies available to lenders. These firms must be capable articulate and therefore analysis variations its decisions. They can’t just say the fresh new AI achieved it. Therefore, the information warns lenders not to ever simply draw packets on the forms in the place of stating this grounds, from inside the for each and every situation, after they change anyone off having mortgage loans. Whenever they never stick to this guidance, he’s offending this new government Equal Credit Options Act. In fact, the brand new Equivalent Borrowing from the bank Opportunity Work need lenders in order to establish the specific reasons for having declining to point financing.

The thing that makes so it? Because when all of our lenders write to us upright-upwards as to the reasons we’re deemed ineligible, up coming we are able to learn how to go-ahead later on, and you can increase our very own borrowing reputation accordingly. And you will, they reassures united states you to definitely unlawful prejudice isnt inside the enjoy. It’s ergo that the CFPB claims the financial institution need to state the brand new detailed conclusions that ran on denial. To put it differently: Stuff performed the brand new applicant manage or not manage?

Including, the newest CFPB claims in its release called CFPB Circumstances Tips on Borrowing Denials because of the Lenders Having fun with Fake Cleverness, a lender need certainly to straightforwardly share the reason, no matter the candidate might possibly be surprised, troubled, otherwise angered to find out they truly are becoming rated on research which can maybe not intuitively interact with the cash.